Pivot Your Retirement Before It Kills You!

A generation ago, IBM did a study of their pensioners and found that their average retiree didn’t make it past the 24th pension check.

John E. Lang, a petroleum engineer and 45-year employee of a single oil company, succumbed to a heart attack in his sleep 10 months after receiving his gold watch – and a few days after receiving a clean bill of health from his doctor. He was my father-in-law – a great man and sorely missed.

Shell Oil studied thousands of its employee and found that retiring at 55 doubled the risk for death before reaching 65 compared to those who worked beyond age 65, challenging the notion that retiring early boosts longevity and, in fact, demonstrating the opposite – mortality rates improve with later retirement.

The National Institute of Health reports that 1 in 5 of the 35 million Americans 65 and older suffer from depression – 2 million suffer from full-blown depression and another 5 million suffer from less severe forms of the illness.

Men older than 65 take their own life at more than double the overall suicide rate and men age 75 and older have the highest annual suicide rate of any age group

OK, can I ask it? Isn’t it time we redefine this retirement thing?

If you are in or approaching retirement, I suspect you weren’t aware of the dark side of this coveted late-life prize. If you have been working with a financial planner, was this ever a part of your discussions with her/him? Not likely – that’s all about the soft side of retirement and, with a few exceptions, financial planners only deal with the hard side of retirement – numbers.

The financial numbers are really important but not if they hasten you into a retirement for which you aren’t emotionally and psychologically prepared. And that’s the rub. Estimates are that 70% of retirees go into their retirement without a semblance of a non-financial retirement plan.

So where can it go wrong?

Ah, let me count the ways. In fact, the husband and wife team of Jeri Sedlars and Rick Miners, veteran executive recruiters and authors of a really good book on this topic entitled “Don’t Retire, REWIRE!” did just that. Following hundreds of conversations with retirees and uncovering this high level of discontent amongst retirees, they compiled a list of the “Top Ten Reasons People Flunk Retirement.” Here’s what they heard the most.

- Retired for the wrong reasons.

- Didn’t realize the emotional side of retiring

- Didn’t know myself as well as I thought I did.

- Didn’t have a plan.

- Expected retirement to evolve on its own.

- I thought rest, leisure, and recreation would be enough.

- Didn’t stay connected with society.

- Expected my partner to be my social life.

- Didn’t know what I was leaving behind.

- Was overcome with boredom.

For better or worse, but not for lunch every day!

Take number 4 and number 8 on that list. This combo illustrates one of the most dominant problem areas when it comes to retirement. The fastest growing divorce rate in our culture is with couples over 50. Couples often fail to plan and consider the impact on their relationship when retirement rolls around for one or both.

For example, the man comes home full-time and the spouse is burnt out on being home full-time. She wants to go her own direction, perhaps even starting a late-life career doing something that has been suppressed for years running the household. The husband has an agenda for retirement, unarticulated until after retirement, and the spouse has different ideas. And gradual separation begins.

I recall a quote from a spouse with a recently retired husband: “I have twice the husband and half the space, and he’s getting bigger. If he rearranges my kitchen drawers one more time, I’m going to kill him!”

It is a little strange.

Couples do quite a job of planning and working their way through other significant life transitions successfully. But with retirement, which is a permanent resident on the top-10 list of life’s most stressful events, couples often ignore planning for it.

The aforementioned stats speak to the dangers of only planning retirement from a numbers perspective. And it’s this evidence and my own personal observations of the dark side development amongst retired friends that have inspired me to become a Certified Retirement Coach to complement my coaching in the area of health and wellness and late-life career transitions.

Time to unwash the brain.

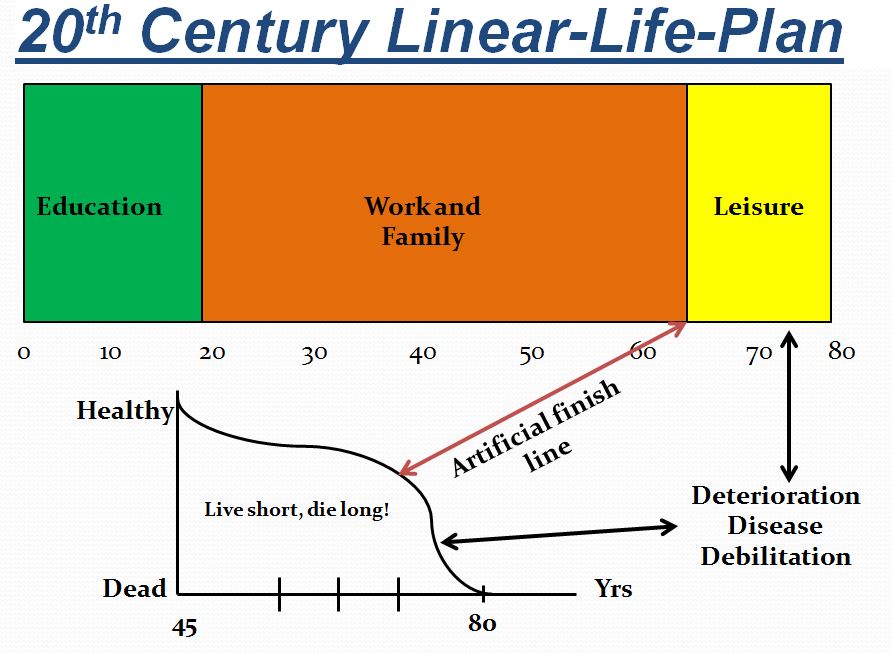

Most of us in the 50+ genre still operate with this linear life plan indoctrination – I call it the 20-40-20 plan that looks like this.

It has been the “social expectation” pounded into us by parents, professors, peers, and pundits: get an education, get a job with a good company, get a spouse, get a car, get a house and big mortgage, 2.5 kids, fenced yard and a golden retriever. Bust your hump for 40 years doing what you marginally enjoyed doing, stretching to reach that coveted final 20 so you can do what you really wanted to do back in the early stages of the first 20. Only to find out that the 20 or so beyond the artificial finish line that our culture establishes isn’t as advertised. In fact, for many, it ends up being a period of decline due to becoming sedentary, socially isolated and functioning without meaningful purpose.

This 20th-century traditional retirement model is a big part of what continues to keep us locked into the “living short and dying long” condition that taxes our health care system and has created a very profitable opportunity for the creators of the massive “warehouses for elders” that are proliferating nationally.

Oh, by the way, I understand there are few nursing homes in Okinawa where elders are venerated and “live long and die short” at home with family.

The solution, please.

Thankfully, the traditional retirement model is dying a slow death, thanks in large part to Boomers who aren’t willing to disappear silently into the night. Research on 55,000 retired Boomers by the Age Wave organization found that only 30% had no intention of ever working again after retirement, while 70% engaged in some level of work, ranging from total volunteer to re-entering the workforce to starting their own businesses.

Successful “retirees” fit a pattern that Mitch Anthony calls the “Four Pillars of the New Retirementality” described in his book “The New Retirementality”:

Vision – successful retirees retire to something; failed retirees retire from something.

Balance – successful retirees find a balance between vocation and vacation; failed retirees move from bingeing on work to bingeing on leisure.

Work is important – successful retirees keep themselves plugged into meaningful pursuits; failed retirees devolve into boredom and aimlessness.

Successful aging is important – successful retirees focus on growing and well-being; failed retirees just take what comes.

Alas, for most going into retirement, this becomes an after-the-fact discovery where productive, healthful time is lost. A Retirement Coach, or a financial planner that includes a holistic, non-financial retirement planning component in their service, can help prevent this dark side of retirement. Dialog on these “soft side” elements should begin 3-5 years ahead of the anticipated retirement date.

Retired or anticipating retirement? Let us help you get it on the right footing. Inquire about our “Retirement Wellness Plan.” Email me at gary@makeagingwork.com.

What’s your retirement experience been? If close to retirement, how much planning on the “soft side” have you devoted to it? We’d love your feedback – scroll down and leave us a comment.

Absolutely the best summary of elements at play in the “3rd act”. Great work, Gary. Thank you.

Thanks Pat.

I find that when you speak to people close to retirement or making the choice to retire their emotional readiness is stifled by the relief of getting away from the stressors they faced daily “on the job.” My antidotal experience has been confronted with first, a person’s unwillingness to enter into dialogue prior to retirement and second, having retired to be faced with some of the challenges you described but now too embarrassed to explore those after the fact. I agree a plan is important and brought into a person’s awareness sometime before retirement.

Thanks, John. Your input as a qualified financial planner is important and a great validation of the challenges prospective retirees are facing. You bring a very interesting perspective on the “roadblocks” new or prospective retirees bring to the table. Look forward to working with you and learning more.

Hi makeagingwork.com admin, You always provide useful tips and best practices.