Aug 8, 2021

Has India Tech’s Golden Decade Arrived?

Retail

Real Estate

Mobile

Finance

Education

SaaS

Series H+

IPO

B2C

B2B

Technology

Last fortnight, India added a record 20th unicorn for the year, almost double in the number of 2020, surpassing the amount of funding raised in all of the last year.

Maine Startup Kyun Kiya

In 1958, India may have just gained independence, but Indians were ready to dream.

Pandit Nehru established the IITs with the vision that they would transform India’s growth journey through technological and engineering innovations. As cliche as it may sound, India’s computer education started there in the 1960s.

In many ways, that is where the seed for India’s Tech Boom was sowed.

In the same decade, FC Kohli was brought in from the Tata Electric Companies run India’s first Tech “start-up”. It was Tata Consultancy Services (TCS) and the year was 1968. The goal for the business was to run as a management and technology consultancy that would create demand for downstream computer services.

Five years later, the first dedicated IT park - Santacruz Electronic Export Processing Zone - was established in Mumbai to promote the export of electronics products and software in 1973.

A year later, India announced its coming of age in the field of technology by launching the first indigenously built computer - TDC-312

The push for “Make in India” v1.0 was inadvertently spurred by a law which to many might seem unrelated to the Tech industry at all. The Foreign Exchange Regulation Act, 1973 imposed restrictions on the use of foreign exchange by Indian citizens and organizations.

This Act made it very difficult for Indian organizations to import computers. Unable to source from outside, the onus shifted to desi manufacturers to mass-produce mini-computers. Shiv Nadar pounced on this opportunity and founded HCL Enterprises, leading India’s push for indigenous hardware supply for computer production.

The Act in many ways made it difficult for IT MNCs to operate out of India.

They diluted their stake and in many cases, exited Indian business. At the same time, the government allowed the import of computers exclusively meant for software export. This step decisively set the tone for the future - “Build in India, Sell to the World”.

As a consequence, IT services firms began appearing on the map. Founders of these companies were educated in prestigious schools in the U.S and had come back to India realising the asymmetric advantage that India holds as an offshore centre.

The IT businesses that were set up nurtured the first batch of entrepreneurs.

Just like the “Flipkart-mafia”, the earliest of the employees in the IT giants of today belonged to Patni Computer Systems.

Private venture capital did not have any established players in India in the 1980s.

Raising a seed round would mean putting one’s own savings to work, and borrowing any additional capital from parents, spouses and friends. Banks would be reluctant to lend to these new startup species.

In fact, Sudha Murthy said that her husband was always in debt, mainly to her.

When the founders of Infosys (all of whom were former employees of Patni Computer Systems) got together in 1968, the company was founded after Mr Murthy borrowed INR 10K from his wife Mrs Sudha Murthy. In those days, the founders worked out of the front room of Mr Murthy’s house.

Little would they know how deeply they would shape India’s tech ecosystem and inspire countless entrepreneurs to dream fearlessly after them.

IT Ki Jawaani hai Deewani

The 1980s witnessed more such waves of IT entrepreneurship in India.

Wipro (by Azim Premji), NIIT (by Rajendra Pawar), Mastek (by Ashank Desai) and many more “start-ups" were established during this time.

The Centre for Development of Advanced Computing set up a National Supercomputer Centre at the Indian Institute of Science, Bangalore in the same decade. Giants such as Citibank and Texas Instruments set up software development centres. Bangalore as an IT Hub started gaining prominence with such developments.

HCL focussed on building hardware for the computer systems. Others such as TCS, Wipro and Infosys focussed on leveraging Indian talent to build software in India and sell to the world.

Before there was SaaS, there was TCS

Pre-liberalisation, India did not have many MNCs who’d buy the products in India, and the traditional family-run businesses were cost-sensitive to pay for software to replace tasks that could be manually tracked.

Regulatory red-tape, license Raj had made India look inward for driving businesses.

Major industries were totally fragmented, and barring a few conglomerates such as the Tatas, Birlas and Mahindras, most other businesses lacked the depth to purchase software. Jio was not even a dream then, and telephone connections waitlist had reached a waiting time of almost 5 years.

Only the software services export market presented lucrative opportunities.

But soon came some sweeping government reforms that threw open the gates of almost every industry to software - banking computerization as recommended by the Rangarajan Committee in the 90s.

Encouraged by the government’s liberal policies, IBM, which had exited the country after the FX Act, came back. GE and Nortel set up the first large-scale offshore development centres. The Y2K opportunity opened up unprecedented opportunities for India—led by its vast technical talent pool and industry-friendly policies.

Its hub - Bangalore.

India’s Internet-first startups emerged right after VSNL launched the first commercial Internet service in 1995, exposing Indians to the World Wide Web and heralding India’s dot-com era.

The same year, Info Edge, one of the earliest Internet companies in India, was founded.

A host of companies across domains had cropped up as well. Ajit Balakrishnan registered the first domain in India and launched Rediff.com in 2001. Shaadi.com, the first matrimonial website was launched.

So was IndiaMart, India’s first B2B marketplace and MakeMyTrip, the first travel and tourism website.

All of these companies had latched on to the trend fairly early.

The Internet was a luxury accessed via dial-in broadband connections. Only a fraction of the population had access to that, but the path ahead was clear. The Internet would rule and software was set to eat the world.

The only question was, when?

Bhaag Dotcom Bhaag

In 99, the word on the street was that if anything had a “.com” as its suffix, its founders were already reaping millions in investor money.

Revenues, let alone profits, were no longer a metric to judge the soundness of the business. Such was investor FOMO to ride onto the Tech boom.

The bubble had to burst, and burst it did, in 2000.

Coupled with multiple Fed interest rate hikes, Japan’s recession and a landmark defeat of Microsoft in an antitrust lawsuit, there was a free-fall in the prices of major US tech stocks. Within a few weeks, all the year-long frantic gains of these Tech cos were wiped out, and many shut their shops even after listing on public markets.

Once the world was back on its feet post the dot-com bust, India was no longer a market that could be ignored. Rediff had just been listed on NASDAQ in 2000, and the world’s biggest VCs were evaluating whether it was the right time for them to bet big on India.

It took a few more years, but ultimately Silicon Valley investors started taking interest in India. In 2006, the first cross-border Indo-US VC fund was set up in India. The angel investing network also consolidated and set up their offices to bet big on India’s Tech.

Soon dealmaking for Tech cos reached a level of frenzy never seen before. The global giants preferred acquiring existing companies instead of building their base from the ground up. eBay acquired Bazee.com, and Monster’s acquired Jobsahead.

India was the next big thing in technology, and it wouldn’t be the first time everyone thought so.

In the same year, TCS, Infosys, Wipro and HCL Tech - all four of them crossed $1Bn in worldwide revenues for the first time. TCS went public, and Google chose Bangalore to open its first R&D centre outside of the US. Yahoo! had done the same thing in the same city, a year ago.

In 2006, Info Edge went public. By that time, it had established several companies under its wings - naukri.com and 99acres.com. Buoyed by the success, the next generation of Internet-first companies was founded.

But soon after the initial rush, VCs figured out even though it was lucrative, the depth of the market was not comparable to that in the US (or China).

India was a heterogeneous market fragmented by diversity and cultural interludes. There were vacuums in the Indian market that had persisted thus far.

Internet penetration was extremely low, the number of mobile and laptop devices combined barely made the optics for the market to be labelled “lucrative”.

The payments and delivery infrastructure were shaky, to say the least. The macroeconomic and demographic trends looked solid, but the present did not correlate.

At the same time, there was no dearth of startups working on making SMS based services in India, which was all that was available to most Indian users at the time. For example, the team at SMSGupShup was working relentlessly to bring Twitter-like group SMSing to life, and the one at JiGrahak was working on SMS e-commerce.

But Apple’s launch of a new iPhone in 2007 triggered Google's release of the beta version of Android, and that marked a paradigm shift that played an important role in shaping the world as we know it.

When the big news of an incoming mobile-first revolution hit the streets, VC’s were asking themselves whether technology was to be inculcated as a core part of a company’s DNA.

A large number of funds, with wallets weighing $150m on an average, had begun their first series of investments around 2007. This also meant that two fast paced years, with a record number of investments made, would follow.

The financial crisis of 2008 marked the flocking of many NRI’s back home, some of which were returning with the specific intention of building global businesses from India.

The blockbuster Flipkart, and the equally prestigious InMobi, were founded in 2007. By the next year, startup funding had crossed $1Bn, and Morpheus, Quickr and Zomato were founded. Another couple of years later, Ola, PayTM and Snapdeal were founded.

The party had just begun.

Lage Raho E-Commerce Bhai

MMT made a dream debut on NASDAQ in 2010.

The new decade marked the establishment of prominent players in other technology-based sectors. The economy was far from ready back then, but the novelty of their idea fetched them high revenues as they progressed. Many of these startups, notable among which are Byju’s, Freshdesk, Zoho and PolicyBazaar, are still sailing on their early mover advantage.

The biggest sector, however, the one that would single-handedly put India on the global radar, was e-commerce.

The founding and the eventual momentum gained by Flipkart brought the conviction that many investment theses counted on. With an increase in expendable incomes on average, Indians were finally ready to place their trust in the online marketplace.

A plethora of startups was working on eliminating the need to physically step out to make purchases, of both daily use and luxury items.

With every store only a click away, the playing ground was levelled, and each new startup competing for the same screen real estate as the other. As trust in the system deepened, multiple players were able to find deeper markets and develop niche offerings for target audiences that were deemed to present “no immediate/real opportunity” only half a decade ago.

The customer was spoilt for choice, and differentiation came from addressing this modern customer’s needs.

By 2012, vertical e-commerce startups like FirstCry in childcare, Lenskart in eyewear, Zivame in lingerie, Bluestone in jewellery and Pepperfry in furniture ended up garnering massive traction.

While mega online stores were also aplenty, their broad-base nature made them more volume-driven, whereas vertical e-commerce players tended to be more value-driven, given the depth of their user research and efforts to curate great products and experiences.

With more consumers shopping online, card payments and NEFT/IMPS transactions grew during the period, opening up the opportunity for the decades-old payment system to be fixed. Expensive credit cards and high friction bank accounts were suffocating the online commerce platforms in India, and a smooth payment experience would bolster the users’ shopping experience.

The building blocks for the payments sector in India were laid by some of the most persevering founders we know of today, one among which is the incredibly tenacious Vijay Shekhar Sharma.

VSS’s PayTM was started as an experiment at the end of the dot-com boom with the three basics of the internet - content, advertising and commerce. The serendipitous pivot came in 2011, when he first pitched the idea of entering the payment ecosystem to his board - a vision he has stuck to, ever since.

PayTM began as a prepaid mobile and DTH recharge platform, incrementally adding new offerings such as data card, postpaid mobile and landline bill payments.

By 2014, MobiKwik and Freecharge had also set up shop by the turn of the new decade, giving their customers e-wallets that let them pay their bills.

The competitors in the payments space spent a lot of time on structuring key partnerships with various businesses in different sectors. It was typical for payments players to partner with banks, but the new tech boom that India was witnessing offered them the opportunity to partner with new-age businesses as well; the likes of Ola, Uber and Zomato.

The payment rails of a startup super train had been set up.

Soonicorns ki Kati Patang

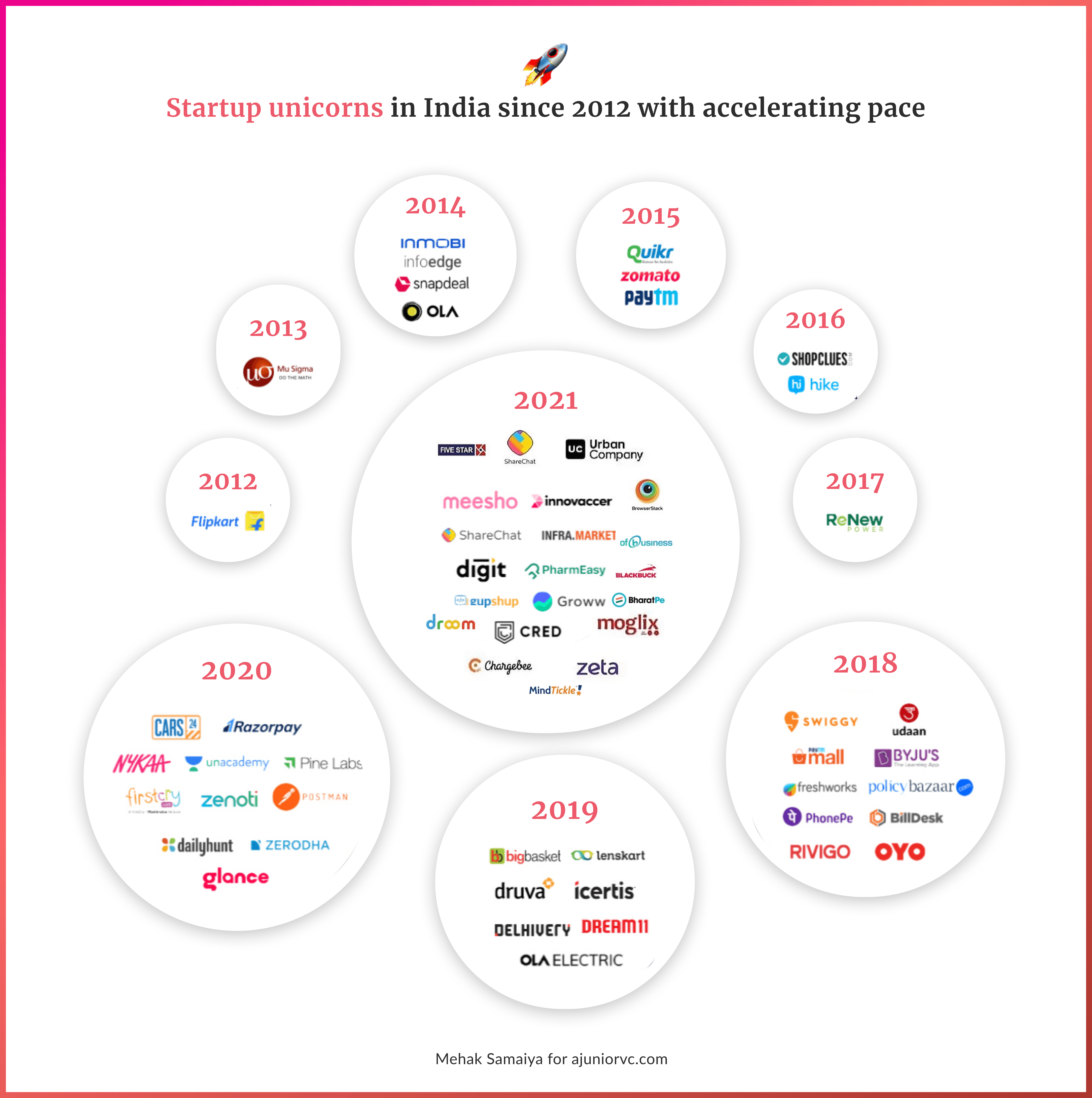

By early 2015, six of the companies had been able to achieve a billion-dollar valuation.

Flipkart, Snapdeal, InMobi, Quikr, Ola Cabs and Paytm all became unicorns. India had just about 350 million internet users as of mid-2015, with ~6 million people being added to the user base every month.

The vast potential in the online purchasing market could be gauged from the fact that it went up to $12.6 billion in 2013 from $3.8 billion in 2009. Google India had projected the number of online shoppers to cross the 100 million mark by the end of 2016.

Jio ji bhar ke

Staring at a seemingly unending market and watching a larger number of buyers being open to online purchasing, the ecosystem recorded mammoth valuations for ventures in this space. It was no surprise that the inflow of interest and capital in this space was at an all-time high.

The market looked so lucrative that the ecosystem saw a record number of investments from angel investors during this period as well, with 650 companies locking in angel investments in 2015 alone.

The grass wasn’t looking as green to some folks, though. Here was born the infamous profitability and cash burn debate.

Critics having serious doubts about the credibility of these valuations noted that the capital inflow was coming in from a consolidated list of 8-10 funds, some of which didn’t even have an India office. These groups were a part of 54% of the deals in the e-commerce space in its nascent stage.

The business models adopted by the ventures backed by these funds, albeit nuanced in their own ways, had a commonality. They all targeted increasing their Gross Merchandise Value, at any cost.

Quite literally.

Fully focussed on earning more customers and top-line growth, companies’ profitability suffered. These companies offered an avalanche of discounts, free shipping, cash-on-delivery with the motive of multiplying their user base, which ate right into their profits. All of this led to direct price wars, where many competitors bled to their deaths.

Some sectors had margins that left room for more than a single player to survive, but many others witnessed a massacre.

The discordance between a loss-making business and a stratospheric valuation was puzzling, and genuine concern about the possibility of it all being a bubble began to float around.

In 2016, the bubble actually burst.

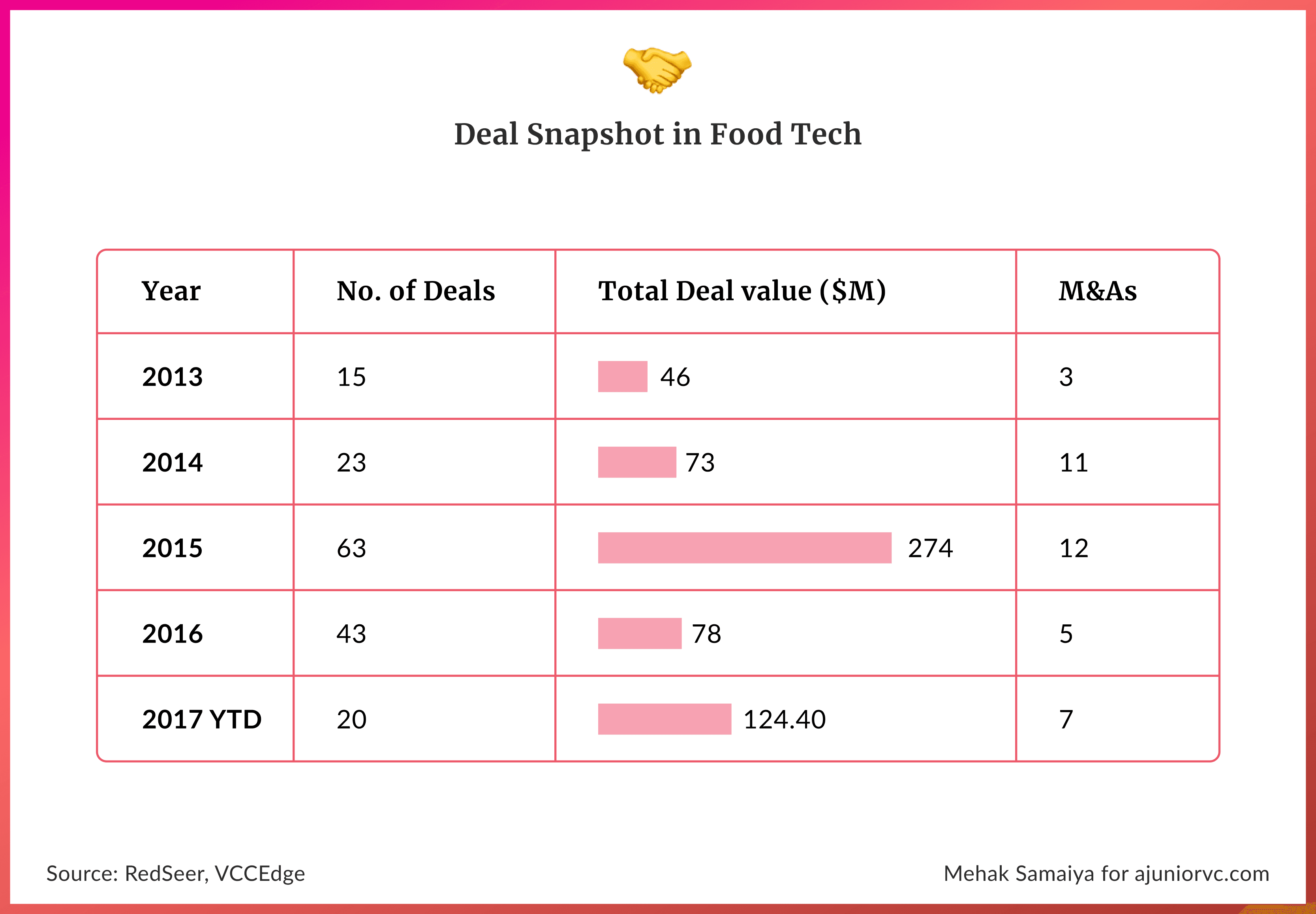

Housing.com went from the apple of the investors’ eyes to a plain liability after a row with investors led to leadership changes and an eventual sale. Freecharge, just after being bought by Snapdeal for $400m was looking at distress sale barely a quarter of what Snapdeal paid for it.

Jabong passed on a $700m offer from Amazon, eventually being bought out by Flipkart for a tenth of the previous offer. Among other high-profile meltdowns was TinyOwl, a food ordering app that was acquired by Runnr, which was eventually acquired by Zomato itself.

Startup funding in the second quarter of 2016 plummeted to $583 million from its recent peak of nearly $3 billion in late 2015.

The ecosystem was facing the first major winter since the funding explosion of 2007. Many began to write off India.

But another large storm was brewing that would alter the landscape for good.

Jio Hai Secret Superstar

The heat from Jio’s explosion began to change the cold winter that had set in Indian tech.

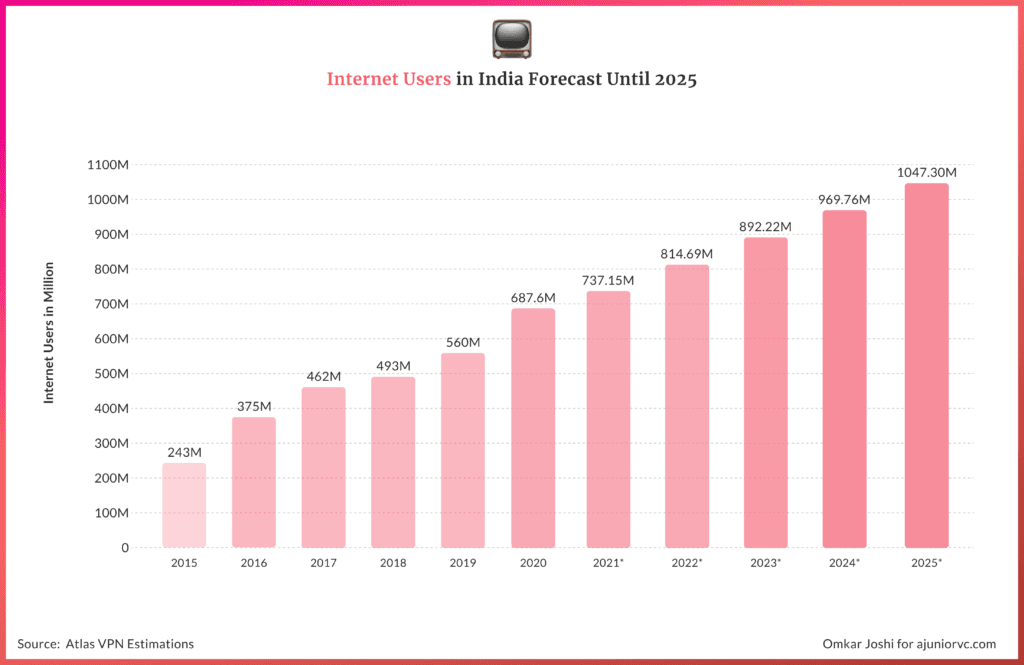

The entry of Jio, took a sledgehammer to the internet data prices. By creating the largest 4G LTE-only data network in the world, at a tenth of the prices, Jio helped push internet penetration in India up from 27% in 2015.

What a bubble looks like

At the same time, online payments were surging. If Jio unlocked data, demonetization unlocked digital payments. The surge towards operating digitally only moved further.

The penetration of internet services in the population, gave rise to unique and India specific consumer demands and gave entrepreneurs an insight into the habits of the next million Indian customers, which brought forward new opportunities that demanded novel business models.

Take agri-tech as an example.

Two-thirds of the Indian population resides in rural settings, a majority of which depends on agriculture or related activities as means of livelihood. Once this population was able to gain access to the internet, it followed naturally that the people would be interested in leveraging its power to better their agricultural outputs.

Seeing this growing interest, companies like CropIn, Stellapps and Agrocart emerged on the scene to help farmers realise their potential.

As for social commerce, it was previously given the cold shoulder because the low internet penetration in the country accounted for a very small TAM.

Social commerce saw not only an interest, but diversification in business models as well. Players like Meesho, Shop101 and Glowroad used the reseller model, where individuals played a role in curating shopping experiences for their network and earned margins on each item sold.

Dealshare used the group purchase model wherein users were given access to a variety of products at prices lower than MRP if purchased in bulk, gamifying the platform experience to make it more captivating. Other ventures like Bulbul chose to include a live streaming model to involve the customer and ease the process of decision making.

Mall91 aimed to fulfil rural India’s shopping aspirations, with their founder noting the whitespace that existed that could now be bridged, thanks to the availability of inexpensive data.

The need for India specific business models inspired a lot of entrepreneurs all over the country to create something unique to solve the problems that Indian consumers faced.

Many first-time founders had understood the problem statements they wanted to address, but not all of them were aware of the nitty-gritties of setting up a business, and many weren’t well equipped enough to navigate the choppy waters alone.

The guidance that these founders needed in the initial stages of setting up their business was

provided by a rising number of early-stage accelerators and incubators. A host of incubators and accelerators such as Cisco Launchpad and Make The Future set up bases in the country.

A growing number of Indian applicants were being inducted into YCombinator cohorts as well.

The learnings could help companies to help lower raw material costs, increase efficiency of operations and improve customer engagement, to name a few areas that often posed challenges.

By 2017, sentiment in Indian tech was turning.

Chak De UPI

India tech’s progression was following a thrilling Bollywood movie, starting slow but becoming tough to keep up.

A collective effort from the Government and the private sector saw to it that the bar was being raised. Over the last few years, giving a billion people an identity was being done with perfection, using Aadhar.

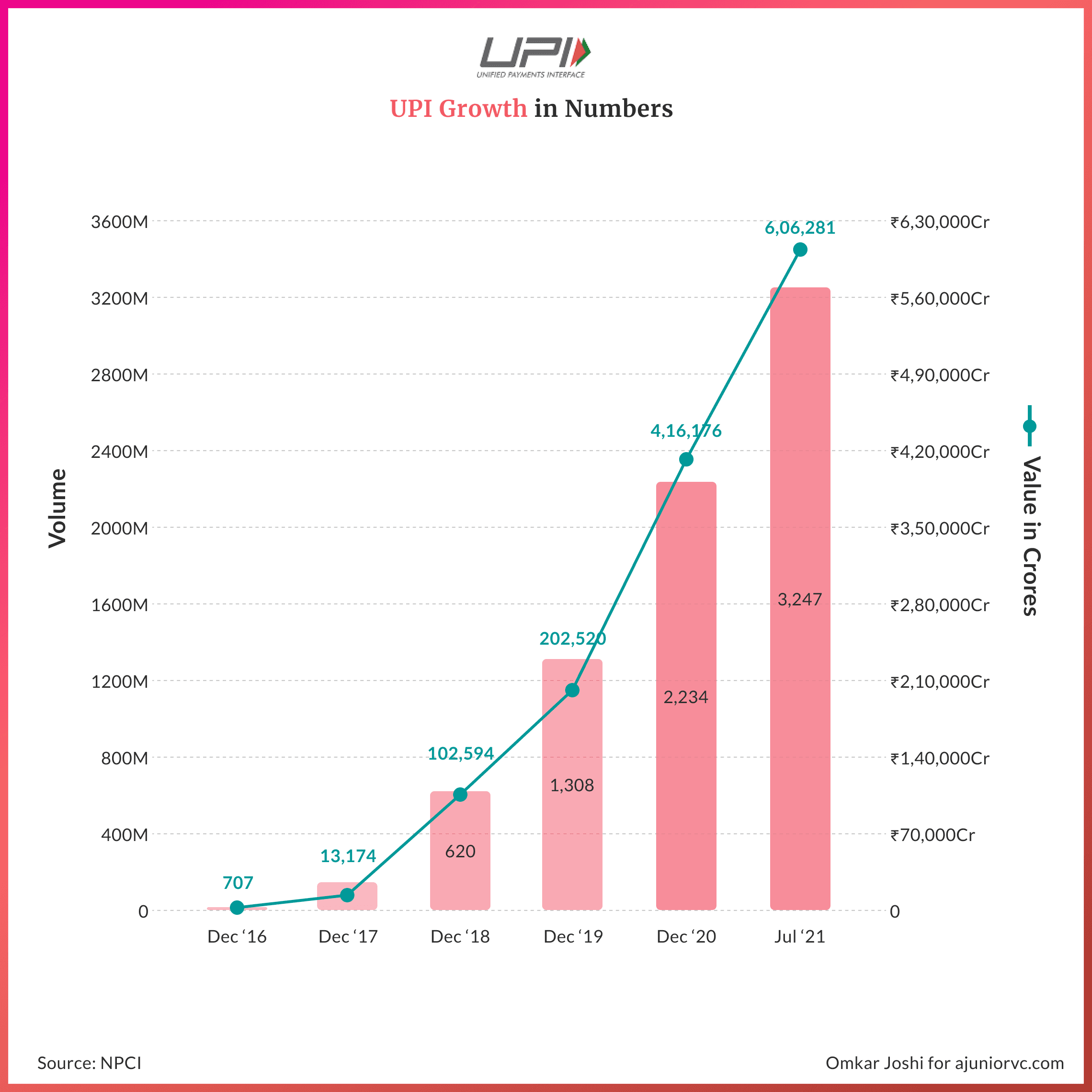

It was now time to use identity to connect people. By 2018, the Indian market was adjusting to the revolutionary payment product Unified Payments Interface (UPI) developed by the National Payments Corporation of India (NPCI).

Hockey sticks are seen outside of the field

This was revolutionary and was not attempted in any other country. Much of the developed world was still using the digital wallet system or the older banking networks.

Now Indians were going to apps like PhonePe, PayTM, and Tez (now Google Pay) for recharging the phone or paying utilities for most of the transactions they did in a day.

UPI created an ecosystem of apps to be more friendly and allow completing transactions in seconds. From an e-commerce site to a Kirana store to an individual, all were now using it due to its ease.

Alongside the Internet was penetrating millions every month, now users could seamlessly transact peer-to-peer from each bank account at scale.

The actual beneficiaries of UPI were India's MSMEs that were so cash-dependent until now, which would slowly start to transform into a cashless system. The sector that comprised 30% of the GDP needed digital solutions for their existing businesses.

This led to many startups coming up and offering a compelling experience built around the already existing payments system.

No western solutions could be replicated. India's playbook was on the cusp to carve its own story, with specialized startups built for the Indian market.

Startups like Khatabook had already scaled to nearly 1000+ Cities in just two years, and BharatPe enabled seamless merchant payments.

Rural India understood that technology was making lives easier and would soon maximize their retail presence by selling on Amazon and Flipkart and new age players like Dukaan.

Food delivery applications like Zomato and Swiggy would penetrate 500+ cities in India. Everyone was experiencing a change for good.

While consumer-facing Industries transformed experience on the outside, on the inside, we were still adapting to the new change.

Business to business would soon help MSMEs go digital in their day jobs.

Zetwerk would help ṭhe manufacturing industry scale-up, while Infra.market would amp up the construction industry. OfBusiness would tackle manufacturing and infrastructure.

To enable all the above functions, the logistics industry, the backbone of the economy Industry, was delivering its expectations and companies like Blackbuck, Rivigo, LetsTransport leading the change.

By the end of 2018 the UPI value grew 700% in the calendar year and had 102,594 crores transactions in December of 2018 alone, highest since its inception.

The confluence of factors of the internet, UPI and logistics was propelling India to a new orbit.

Andaaz India Stack Ka

The ability to connect more people was India’s task, and Jio was executing it at scale in 2019.

Every month it was adding over 10MM new subscribers in 2019 to its already existing 100MM subscribers. To give context to the numbers, the population of Sweden is 10MM.

Talk about literally adding a country.

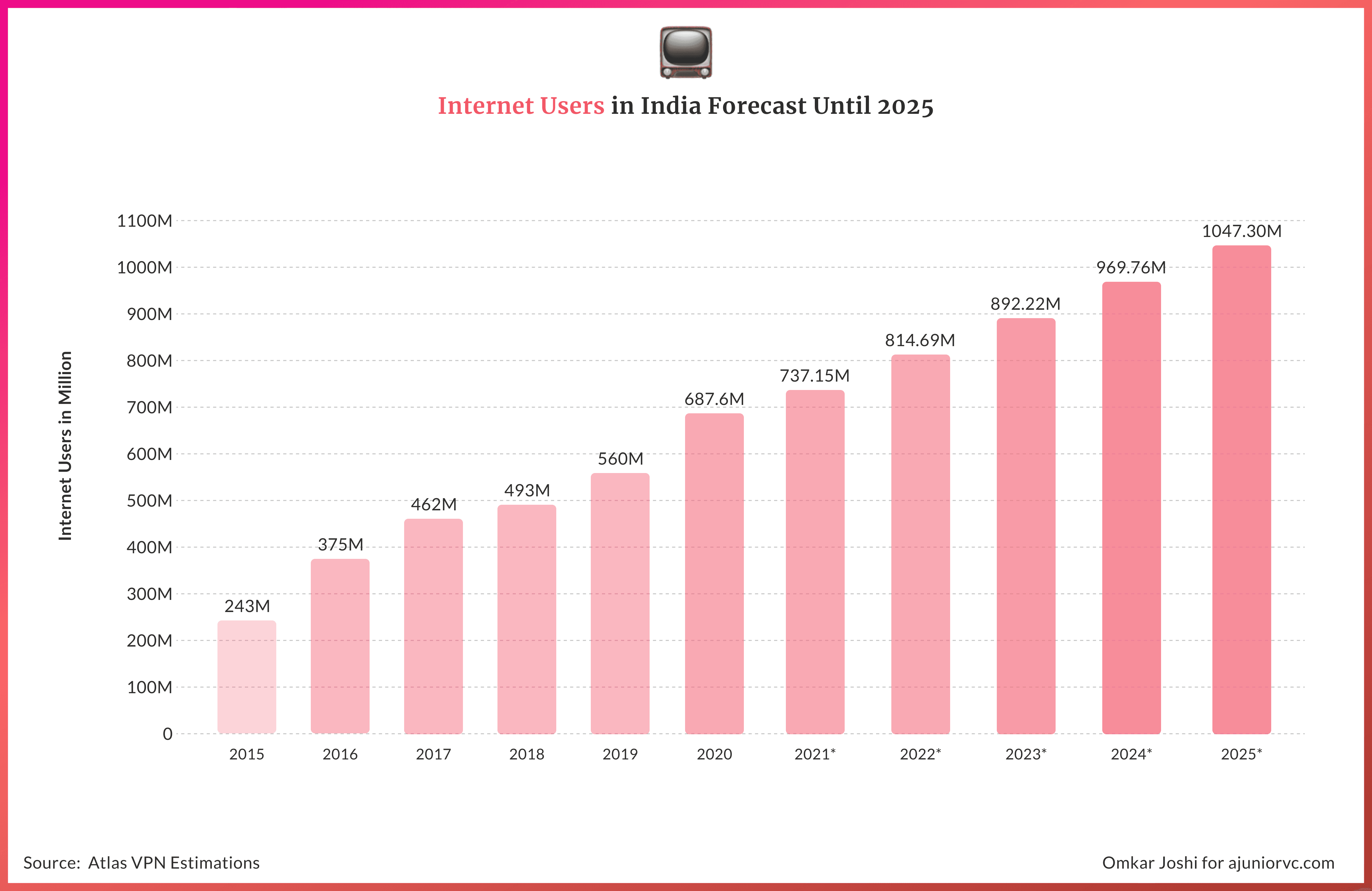

Internet penetration is an indicator to showcase access to the digital world. It was 7.5% in 2010, grew by nearly 4x to 27% in 2015 and jumped to nearly 49% in 2019.

Internet penetration only made sense if the data costs were low. India's data costs were the cheapest by a huge margin at $0.09 per GB and compared to the US that was nearly $8 USD.

While the internet is the channel to connect, the smartphone is the tool. This device connected a billion people with just a touch away. We had over 350MM smartphone devices by the start of 2019.

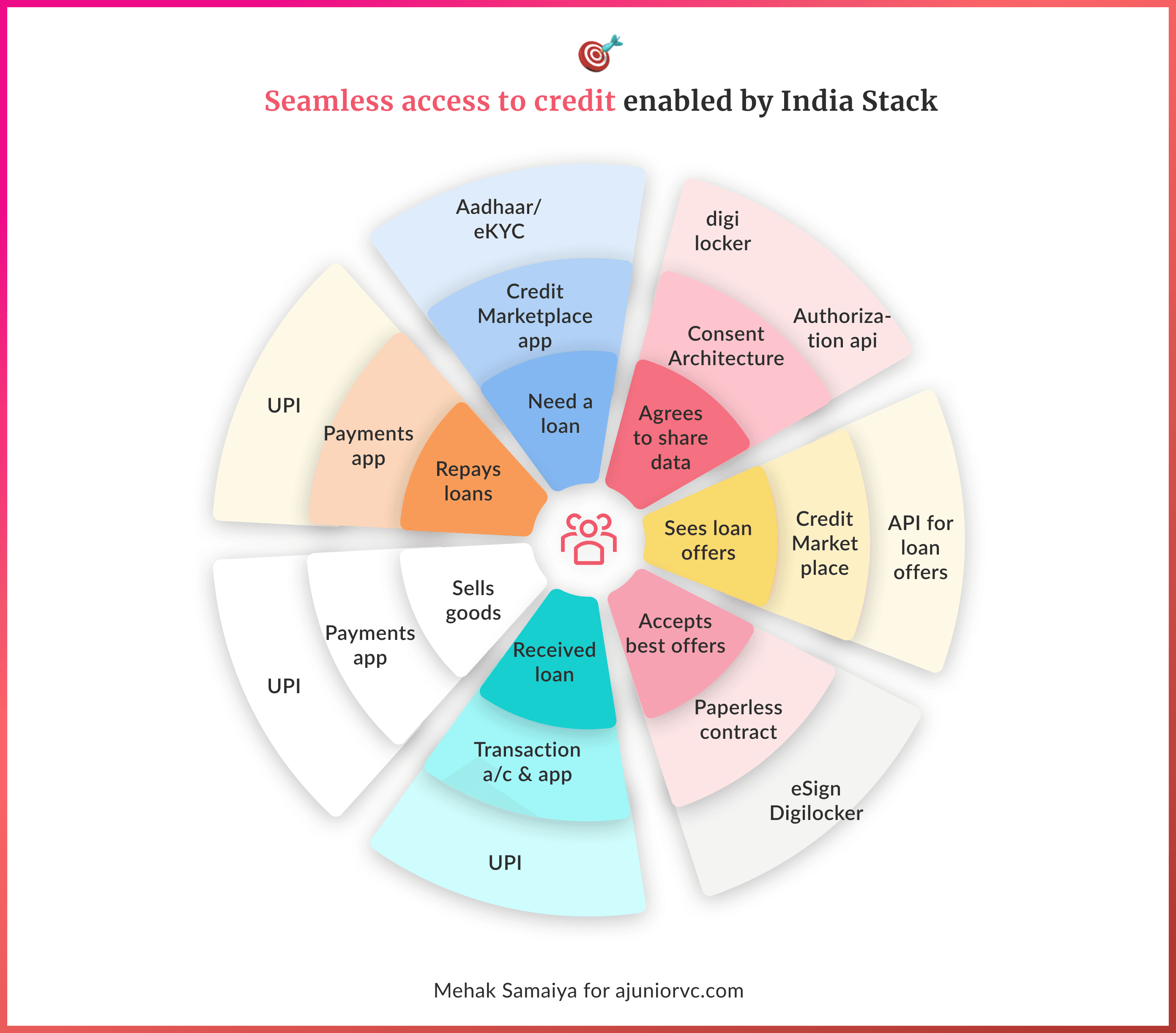

All this was possible at scale with the initiative taken from the government's front on the India Stack with UPI, Digilocker, Aadhar, and E-sign. While the government was doing its part, the start-ups were also pushing their limits.

Start-ups were both building for India as well as exporting the products to the western markets.

Companies like Freshworks started maturing and had reached $100MM ARR. Zenoti’s 65% of business came from the US market.

India truly exported software at scale, just like how they started providing IT services two decades ago.

India’s average age was 26, and we were not only good at tech, but our habits and needs were also young. Nykaa, a D2C fashion brand had turned profitable with an annual revenue of ~INR 1160 crores.

India’s very own fintech game was getting stronger by the day, and start-ups like Razorpay, considered to be Stripe of the East and Pine Labs, a PoS Payment Solutions, had entered the Unicorn club.

Right when start-ups were exceling, the government did not stop innovating.

Most of the start-ups were providing great solutions to the users, but understanding the user information and accessibility of credit was still developing in India.

Even before the start-ups could make their own solutions, the government's Account Aggregators and Open Credit enablement networks would have its adopters.

Now Indians could share data, provide credit, and do the background check with consent with a click of a button. This was pretty revolutionary as developed countries like the US, France, Germany and UK were still using paper systems to share data while we were acing the data game with just our fingers.

Our India Stack now seemed complete. While the world was wondering how India pulled this off and replicating India stack, India was marching forward.

Right when things were going great, disaster struck the world. Covid-19 pandemic had started affecting India at mass. Now everyone was forced to adopt a tech-first approach.

While the start-up adapted well, the users adapted even better. Our strong foundations of the internet kept us intact and by the end of 2020 we had 36 unicorns.

But who knew what 2021 was about to bring.

Tech Baahubali

If Rocky's Gonna Fly Now had a reference, it would be India's 2021.

We are in the midst of a blockbuster year for Indian tech. Indian startups raised a total of $22.6B just in the first 7 months of the year, making it the highest in the history of India. The Unicorn party had started and it was roaring with 6 unicorns in 4 days in Apr 2021!

India had zero unicorns in 2010, four in 2015, and by midway of 2021, we will have 57 with 20 new ones being born in just the last 7 months.

Unicorn pawri

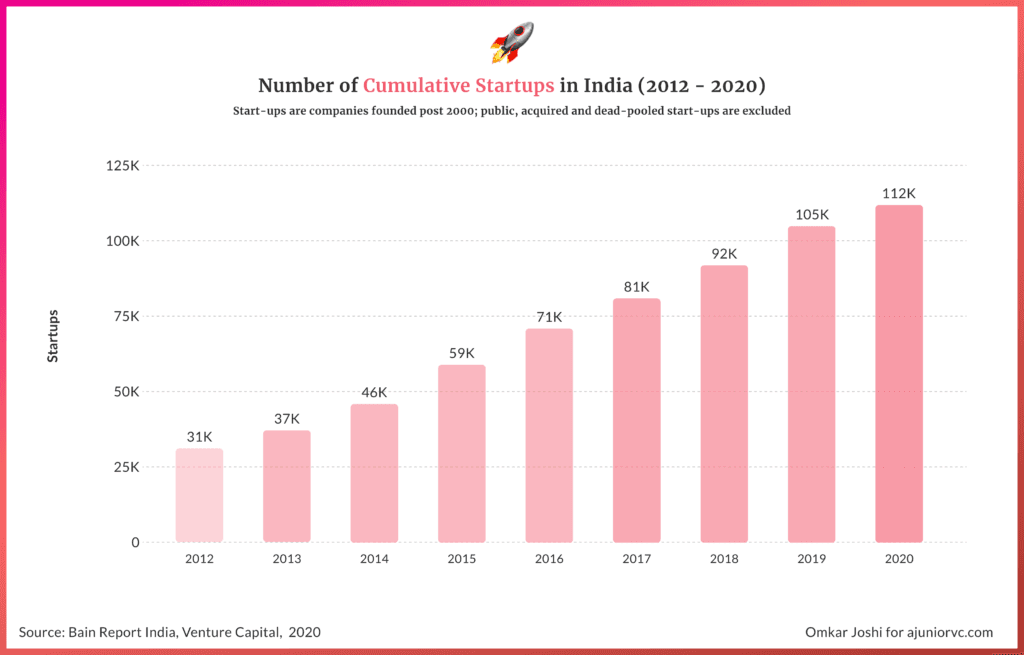

Overall, India had 47,000 startups registered with the government of India – that promises hundreds of unicorns from the larger scheme of things

While unicorns have rolled eyeballs for many Indians, for some, it was just terminology. Critics have often referred to some of these companies still losing money. Albeit, now these companies would strive to build value for their users, investors, and shareholders.

They are also bolder and more ambitious now with 4-5-year-old tech startups acquiring decades-old incumbents.

The above ingredients have paved the way for the startup India we have worked for over the two decades. The next step is to reward the shareholder who believed in the startups with just an idea on a piece of paper and backed it through the journey.

Exits have been a huge question mark for investors trying to invest in India. Lack of scalable business models, mature teams and tough policies crushed all these hopes.

Unlocked by startup-friendly policymaking, the decade forward looks bright.

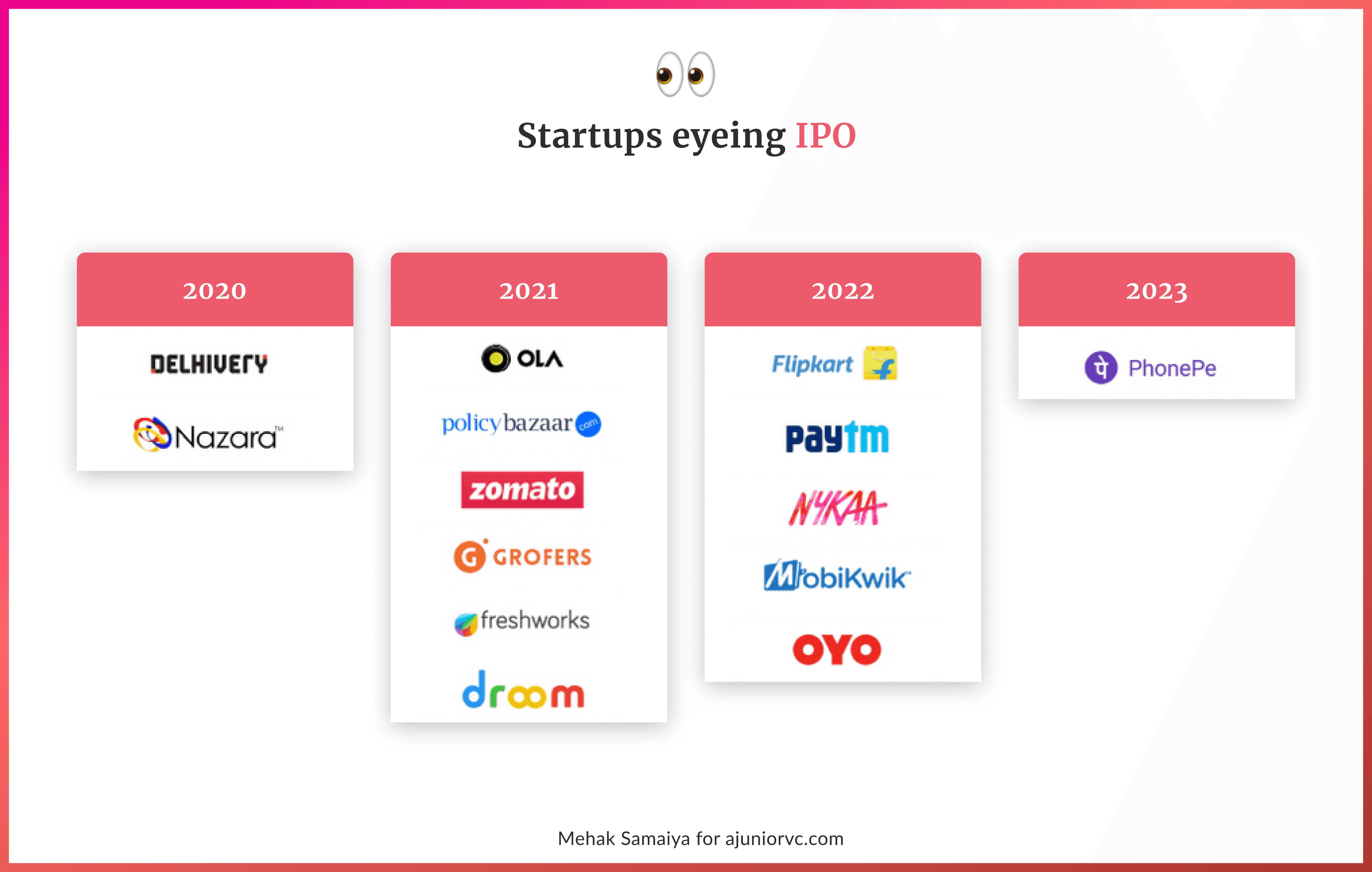

2021 onwards is the inflexion point for new-age Indian technology startups 2.0 to reward themselves, their investors and the Indian public that believe in these firms with the bandwagon of the Initial Public Offering.

While new-age early technology start-ups have already listed, the gains for their investors and the founders have considerable.

Ceteris paribus, while we have the channel and tools, the growth engine will start to truly spin only when the income and consumption increase with our own indigenous firms.

Many start-ups that understand the Indian mentality would erupt, solve for the next billion internet.

Today the user gets the experience on the big-tech products from the west as data is curated, and personalisation will be the key for these products. We would see the same for the upcoming start-ups in India.

Much of the upcoming generation will seldom use cash to transact. Fin-tech may well be our greatest strength. While parts of the world will still be using cash and coins, we will only transact in a digital form of currency.

On the export front, the world would continue to use Indian software due to the high product quality, low cost, and English speaking customer support that Indians provide. Software-as-a-Service alone would account to be $1Trillion.

Deeptech and space-tech research would be mainstream from India due to the tech advancement and low cost infrastructure that we have built.

Overall, Indian market is so vast, that no one player will add value in each sector, there will be players serving in all sectors for all kinds of users.

Itching to contribute to India's glory days is a Swades moment for Indians living abroad, and many are taking a one-way ticket to India.

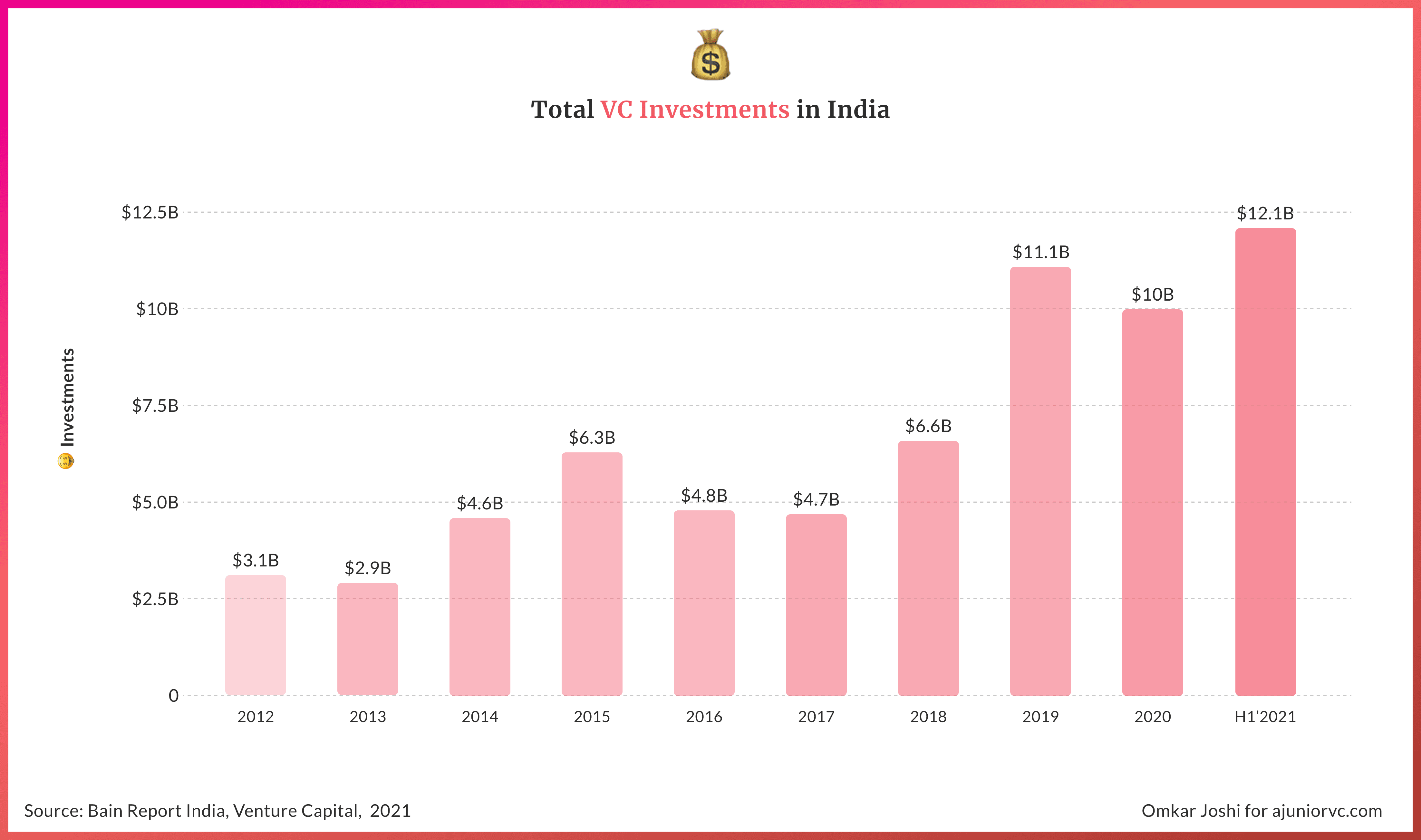

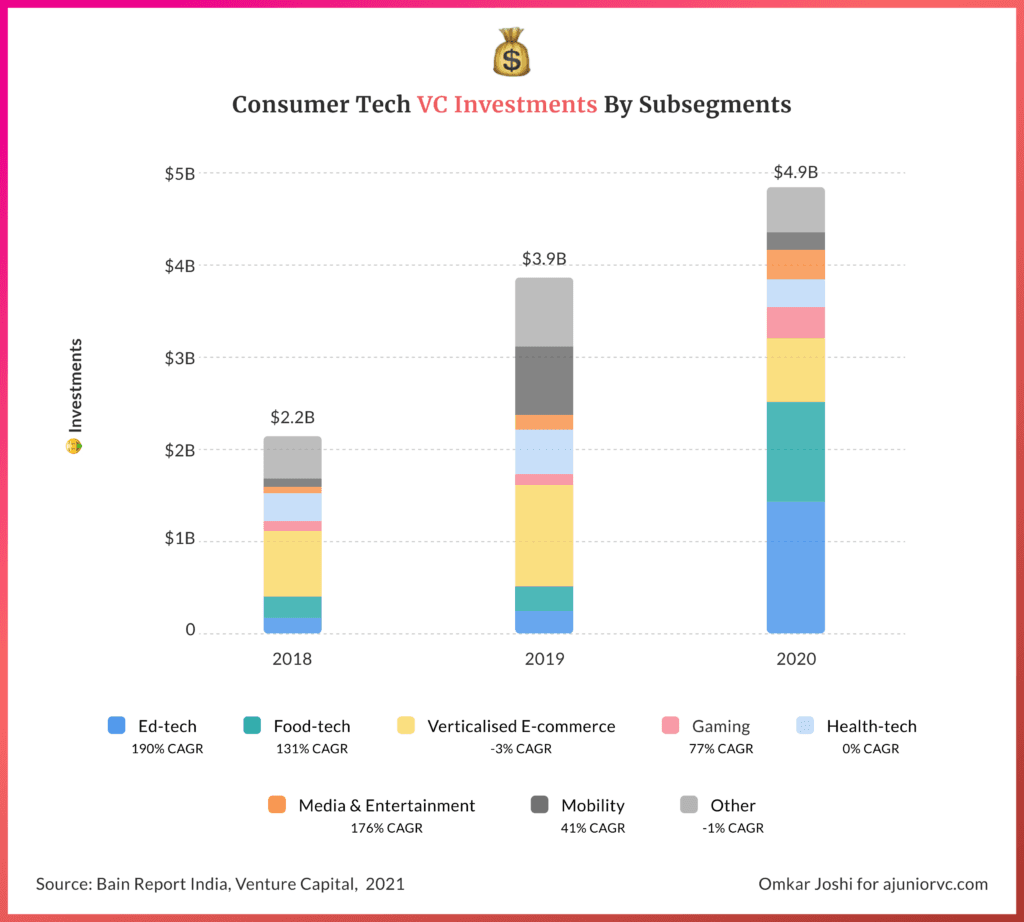

The next decade is potentially going to be the biggest for Indian tech. With $12Bn already having been infused in Indian tech, we are on track to 2x of 2020.

Internet penetration, smartphone penetration, UPI, logistics have formed the backbone for Indian e-commerce to thrive. Policies for investing, doing business and exits have unlocked gateways for a flood of capital. With China tech closing up, India becomes an even more lucrative tech market.

With the world’s largest young population added to this, we have the trifecta of labour, infrastructure and capital. There now seems to be little that could stop India.

After decades of having settled for no medal, the next decade could be where India tech finally hits Gold.

Authors: Bhoomika, Keshav, Raj, Shreyans, Aviral Design: Saumya, Mehak, Omkar